Notes on DML for DiD: A Unified Approach

Introduction

This blog post explores how Double Machine Learning (DML) extends to conditional Difference-in-Differences (DiD), focusing on doubly robust estimators. The key insight is that conditional DiD can be understood through the lens of cross-sectional ATT estimation.

Foundation: Cross-Sectional ATT Estimation

To build intuition, we start with the familiar cross-sectional setting. Standard identification requires three assumptions: SUTVA, unconfoundedness, and overlap.

Step 1: Propensity Score Approach for ATT

-

Unlike ATE, ATT estimation requires only “one-sided” unconfoundedness and overlap conditions.

Assumption 1 (Identification Assumptions).$$Z \indep Y(0) \mid X \text{ and } e(X) < 1$$ -

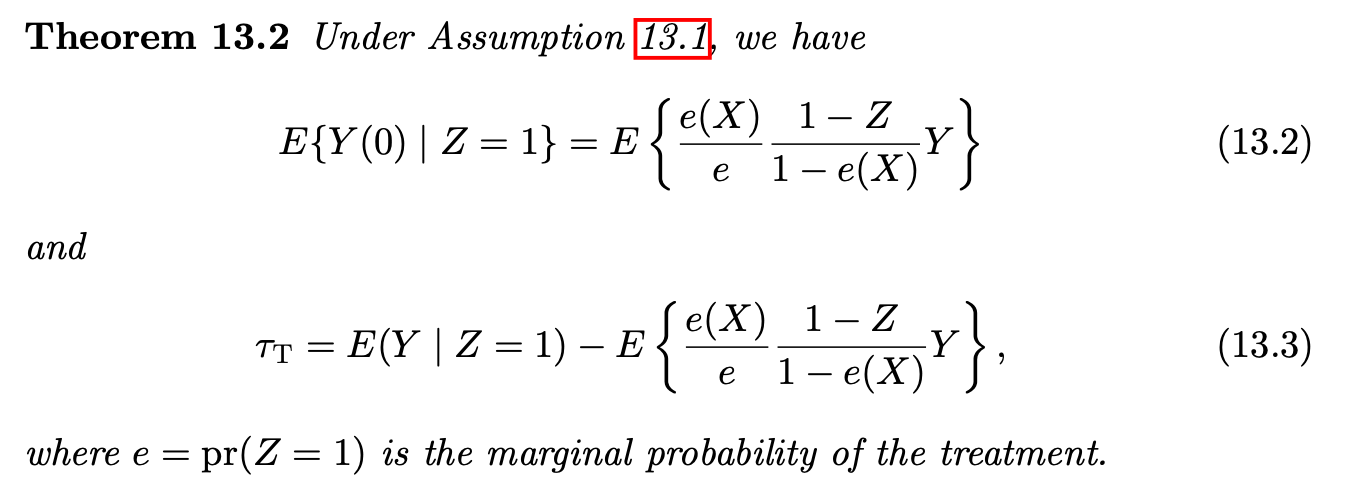

Estimate ATT using IPW

Theorem 1 (Ding (2024), Section 13.2).

-

More general, Li et al. (2018a) gave a unified discussion of the causal estimands in observational studies.

Theorem 2 (Ding (2024), Section 13.4).

Summary Table of common estimands:

-

This table provides us a good way to understand and remember IPW estimator for ATT

-

How to remember $\tau^h$? Apply IPW on “pseudo outcome” $Yh(X)$ then divide by $E(h(X))$

-

When the parameter of interest is ATT, then $$E(h(X)) = E(e(X)) = E(E(Z \mid X)) = E(Z) = \P(Z = 1) = e$$

-

Use it to better understand IPW for ATT

-

Step 2: Doubly Robust ATT Estimator

-

Combines outcome regression and IPW methods

-

For DR estimator of ATT, check my previous post

-

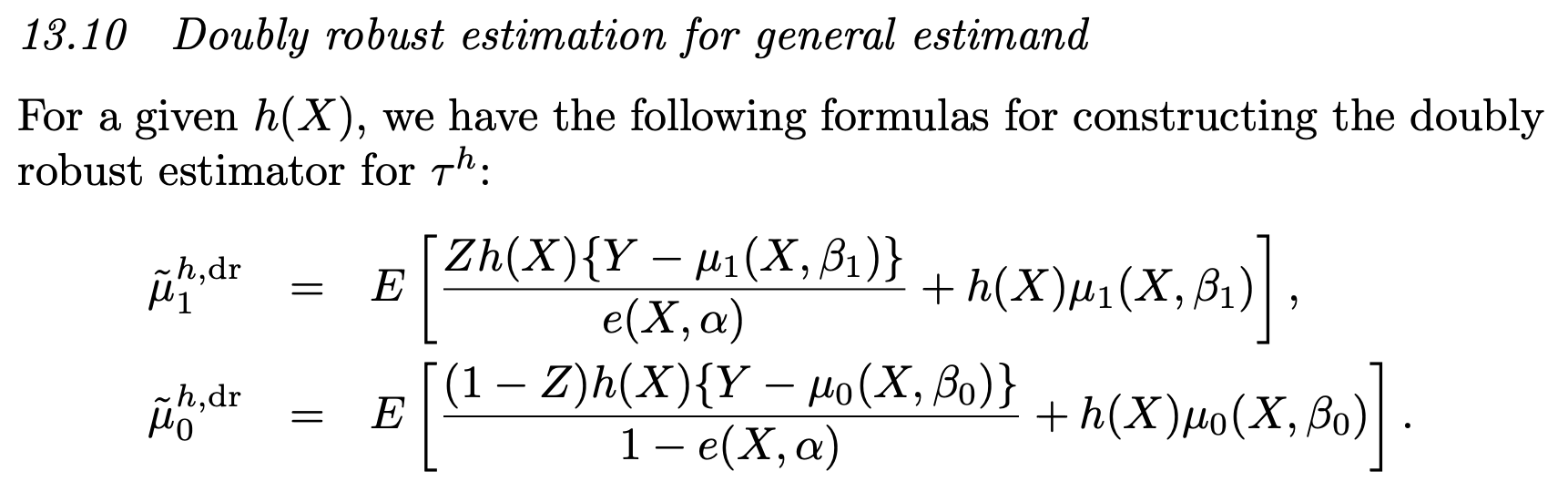

More generally, we have

Theorem 3 (DR for general estimand, see Ding (2024), page 191).

Extension to Conditional DiD

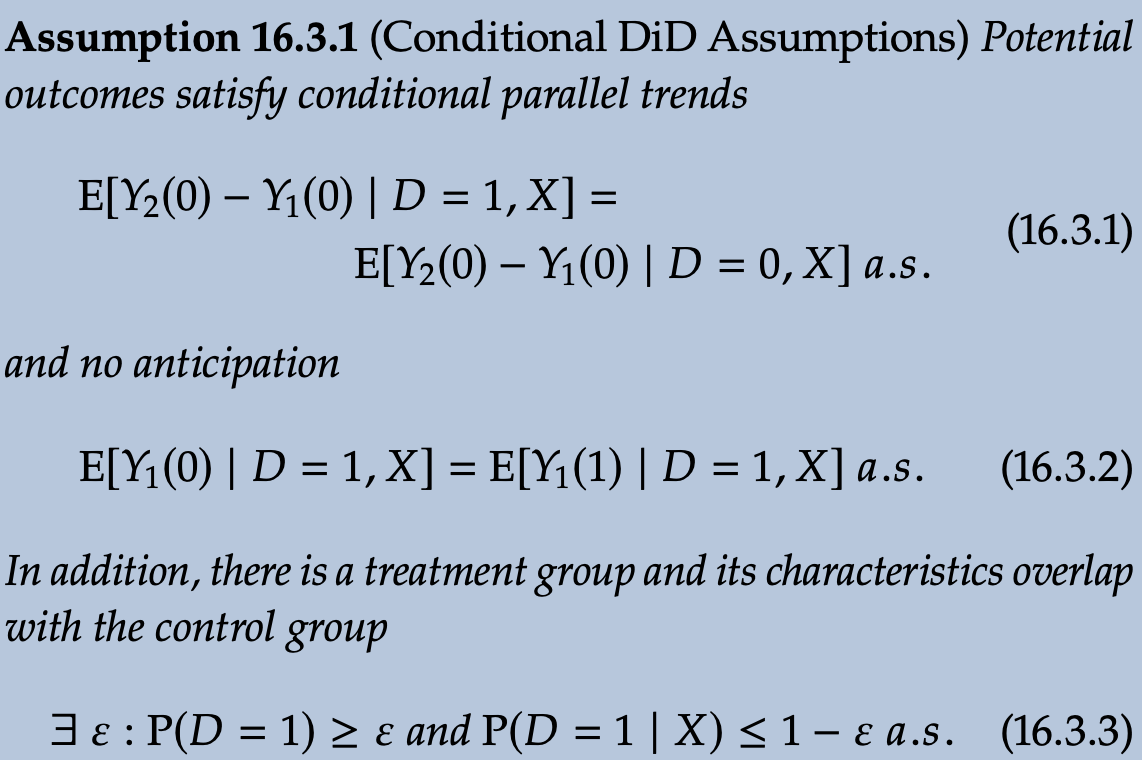

Identification Assumptions

Conditional DiD relies on two core assumptions: conditional parallel trends and no anticipation, plus an overlap condition.

- How to understand the overlap condition (16.3.3)? It essentially imposes that there are control observations available for every value of $X$.

The Key Insight: Transformation to Cross-Sectional Problem

By taking the difference,

$$ \Delta Y = Y_{\text{after}} - Y_{\text{before}} $$

we transform panel data into a cross-sectional problem. This allows us to apply the same doubly robust framework used for cross-sectional ATT.

The Unified Result

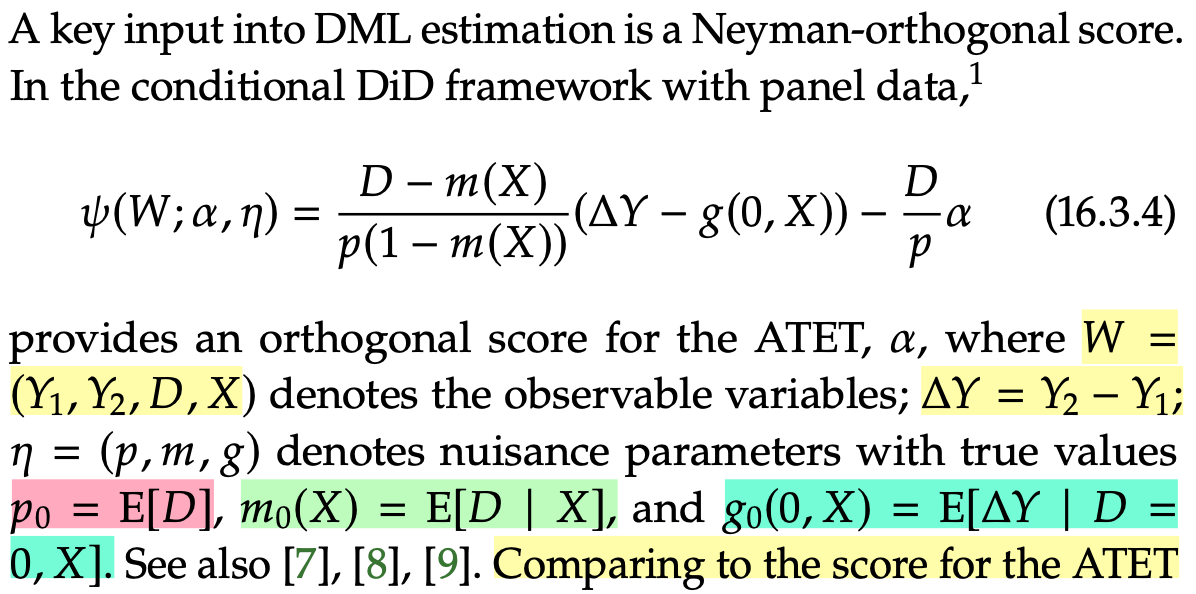

The Neyman orthogonal score for conditional DiD is identical to the cross-sectional ATT score, where the outcome variable is simply the difference $\Delta Y$.

-

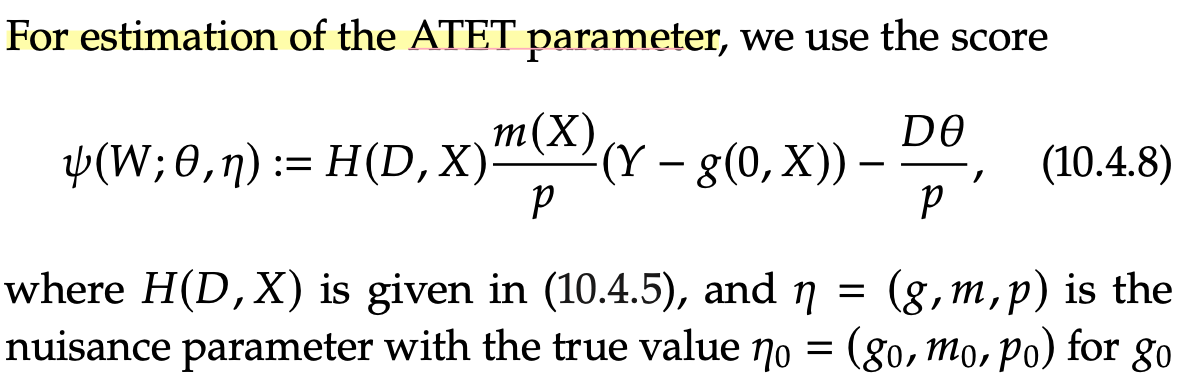

Neyman orthogonal score for ATT in conditional DiD

Proposition 1 (see CausalML Book).

-

Neyman orthogonal score for ATT in cross-sectional setting

Proposition 2 (see CausalML Book).

-

Comparing to the score for the ATT in cross-sectional setting, we see that DiD score is identical to that for learning the ATT under unconfoundedness where the outcome variable is simply defined as $\Delta Y$

References

Chernozhukov, Victor, Christian Hansen, Nathan Kallus, Martin Spindler, and Vasilis Syrgkanis (2024), “Applied causal inference powered by ML and AI.”

Ding, P. (2024). A First Course in Causal Inference. CRC Press.

Callaway, Brantly and Pedro H. C. Sant’Anna (2021), “Difference-in-Differences with multiple time periods,” Journal of Econometrics, Themed Issue: Treatment Effect 1, 225 (2), 200–230.

Chernozhukov, Victor, Whitney K Newey, and Rahul Singh (2022), “Debiased machine learning of global and local parameters using regularized Riesz representers,” The Econometrics Journal, 25 (3), 576–601.

Chernozhukov, Victor, Whitney K. Newey, Victor Quintas-Martinez, and Vasilis Syrgkanis (2024), “Automatic debiased machine learning via riesz regression.”